What Happens When Founders Can't Raise But Don't Want to Lose it All

Participants at the Harbottle offices for the founder roundtable

When Chris Kirby and his co-founder were fundraising for Tomorrow's Journey Series A a few years ago, his pitch deck and financial model he presented to VCs projected the startup growing from £1m to £37m in five years. You know, the typical hockey stick chart founders are told represent ‘venture scale’ and that are absolutely essential to nail down term sheets.

Their bold approach worked! They received three term sheets of between £3 million and £5 million. But something didn’t sit right with Chris. He realised that the projections were ridiculous, and so was the expectation from investors that he’d spend funds raised very quickly. So he did the unthinkable - rejected all the term sheets and walked away from the venture path.

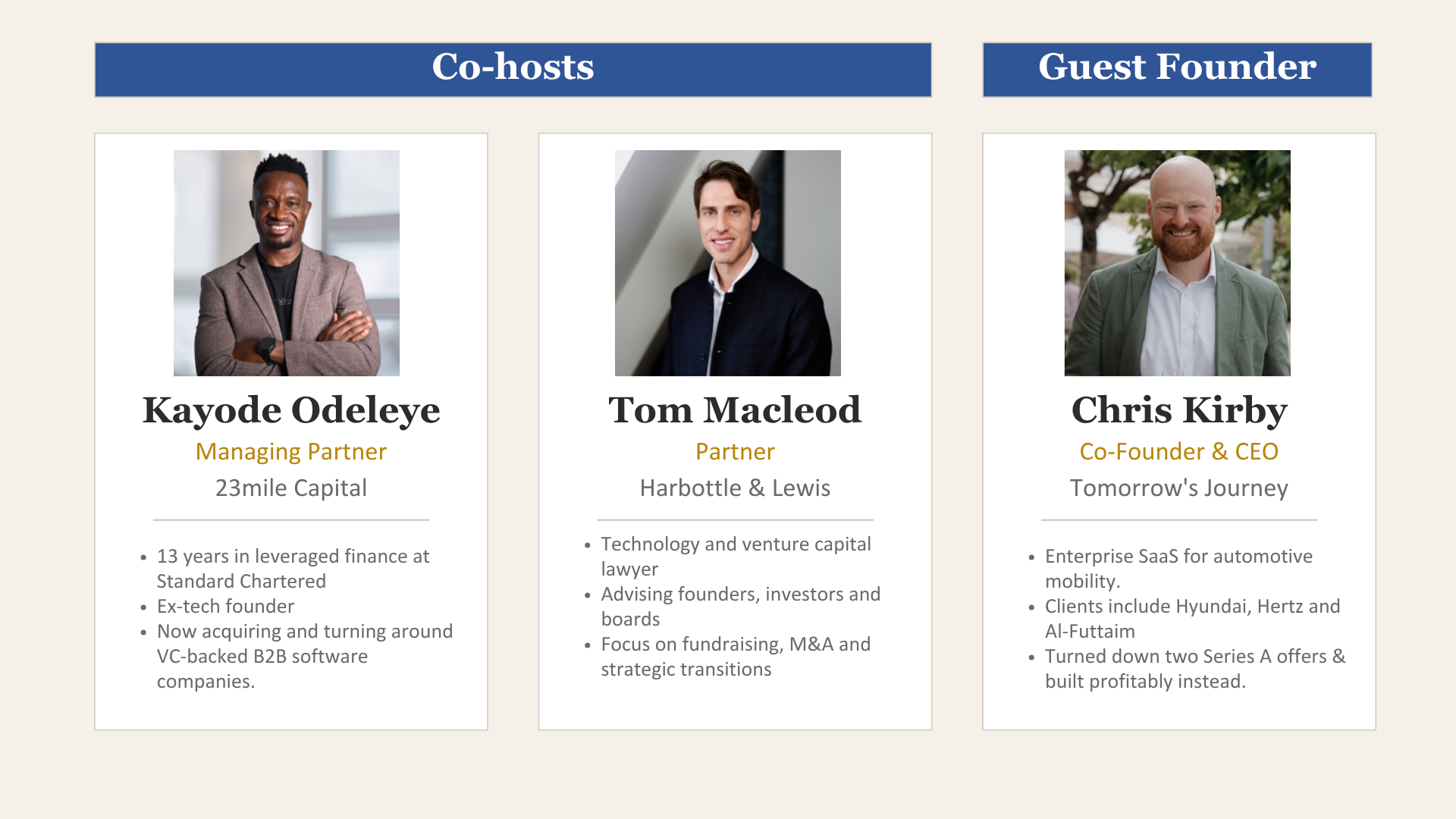

Chris shared this story with a room of venture-backed founders at a curated breakfast workshop held at Harbottle & Lewis's Strand offices on 31 March. Co-hosted by Tom Macleod from Harbottle's venture team and Kayode Odeleye of 23mile Capital with Chris as guest founder. Every founder in the room had raised between £500k and £5m, and several were in the middle of rethinking their capital structures or planning for exits. The conversation that followed was honest in a way several attendees said they struggle to find, even within their own boards.

Co-hosted by Tom Mcleod and Kayode Odeleye with Chris Kirby sharing his journey rejecting venture capital

Here’s a quick recap:

UK Venture Overview

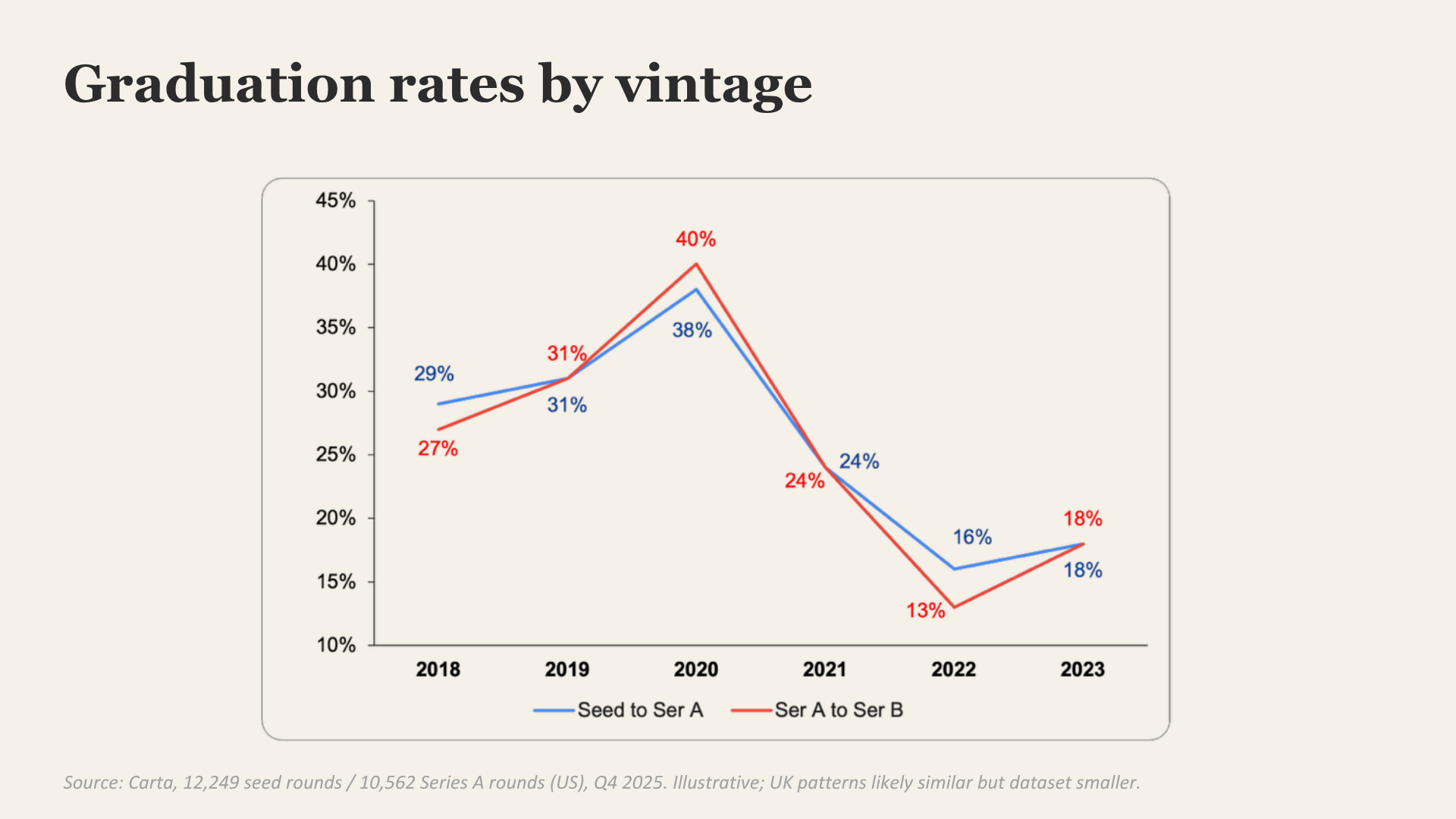

VC fundraising is down 81% from the peak, and most of what's still being deployed is going to AI. Carta's graduation rates from Seed to Series A and Series A to Series B have converged at around 18%, which means roughly 80% of venture-backed startups are not raising a follow-on round within two years. The data is US-based but the UK picture is similar or worse.

US based startups raising Series A (Red) and Series B (Blue) within two years of previous round

The tough fundraising environment is driven by two things. The internal version is that hitting the targets you projected is harder than it looked on the pitch deck, because raising more money doesn't make an enterprise customer respond faster and it doesn't create a market where there isn't one. The external version is that founders hit every target and still get caught out, because VC interests have shifted or the bar has moved.

We walked through an experience of a founder that raised £3 million to scale a profitable business. VCs pushed for her to scale fast, so the team hired tons of staff and spent aggressively on marketing. Impressively, they grew 180% year-on-year to reach nearly £7 million in revenue. They proudly presented their metrics to the board and requested commitments to raise a Series B, but were met with the shock of their lives. The same VCs that promised follow-on funding if they met their numbers withdrew support because their fund thesis had changed. The company was forced to embark on a restructuring to save what they’d built over a ten-year period. In this case, the founder delivered on their side of the bargain while the market changed around them.

Default Options: Scale Fast or Die Trying

The default journey for venture-backed founders: scale fast or die trying

We had concrete examples in the room of founders who had forged their own paths. One founder had raised several rounds entirely from angels, each on favourable terms, without ever touching the conventional VC path. Another had been running her startup for 12 years and at one point returned cash to investors because they didn't want the pressure of chasing targets that would take them away from the social mission they were committed to. Kayode and Chris had a live fireside conversation running through Chris's experience rejecting VC, the challenges that came with that choice and the benefits he's seeing years down the line.

Getting there isn't straightforward, because a theme that kept surfacing was the gap between what founders expect from their investors and what they actually get. One founder had raised a lot of money and expected the investors to be supportive, the so-called value add. The consensus from the room was that the best you can realistically hope for is the money itself, and for them to leave you alone. Most of the time, especially with VCs, investors are more likely to be disruptive than helpful.

The same point applied to venture debt, where the non-dilutive argument is real but repayment is the trap. Most founders take on venture debt assuming they'll raise the next round to cover it, and when the next round doesn't come, the debt becomes very hard to service.

Three Non-Conventional Paths: M&A, Alternative Financing, and Pivoting to Profitability

Non-conventional options VCs and board members don’t offer to founders

Chris's story has a chapter that makes the M&A path real. A couple of years after he turned down the Series A term sheets, he came close to selling Tomorrow's Journey. He signed a term sheet with a much larger startup valued around £1bn, with the deal contingent on the acquirer closing their own round. Six months in, their fundraise fell apart and the deal collapsed with it. Chris's business took a hit because they'd run up costs expecting the money was coming, and they had to cut back hard before getting the company back on track.

Tom picked up the M&A conversation from there and made a useful distinction between trade buyers and financial sponsors. Trade buyers will often value a company on more than just revenue, because they might be buying for the product, the technology, or the team. Harbottle is seeing more acqui-hires lately, which tracks with this.

There's a related point that a lot of founders miss: there's more to sell than financials. For the right acquirer, the product or the team might be worth more than the revenue line, and getting that positioning right is where advisory experience matters. Tom also flagged something that keeps happening, which is founders trying to run the M&A process themselves. It's a full-time job, and the moment it becomes the founder's main focus the business and the numbers start to suffer, which weakens the deal at exactly the wrong moment. An experienced adviser can run the process while the founder stays focused on running the business and hitting targets.

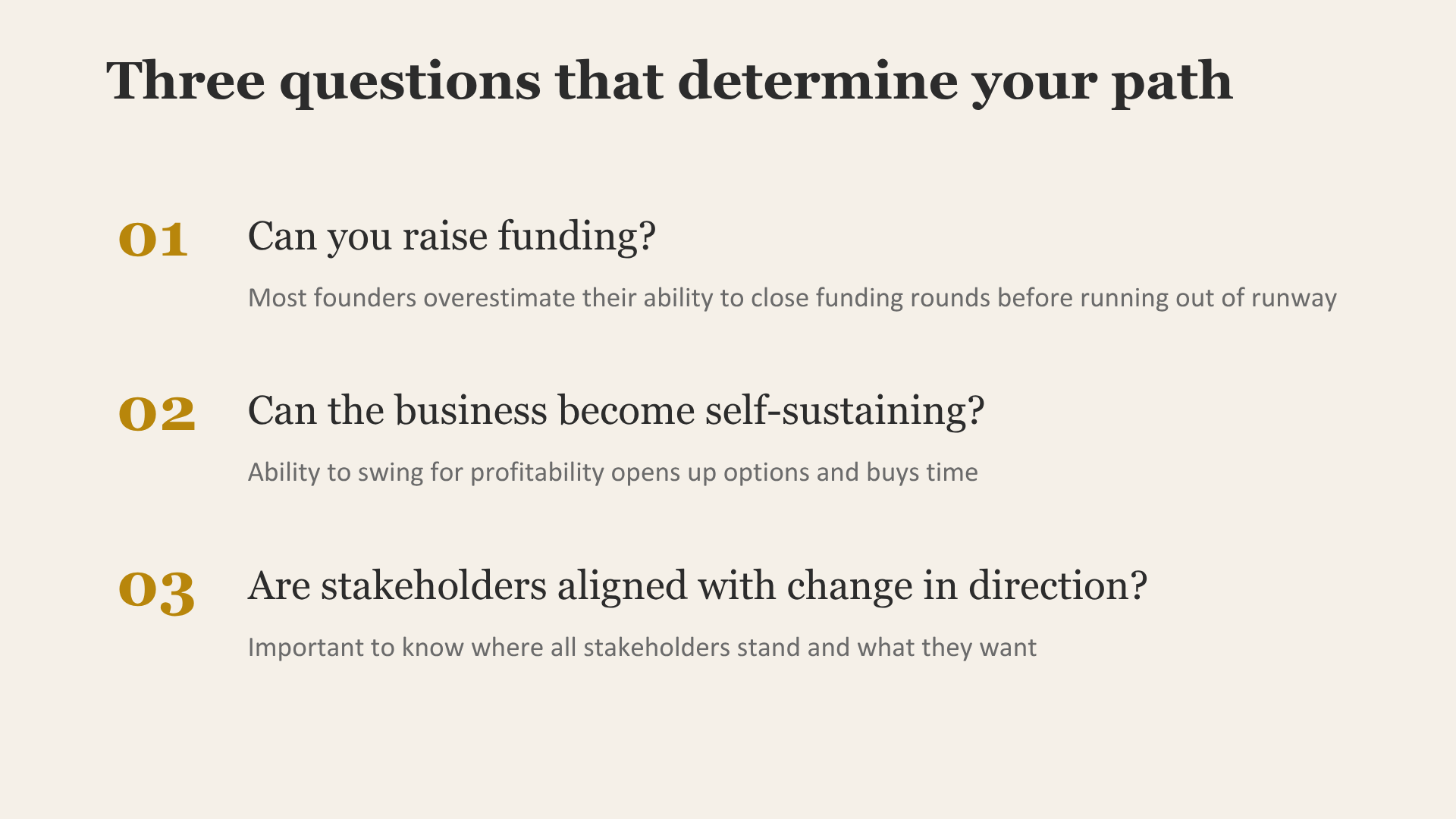

How Do You Know Which is Right For You?

The first is how much runway you have, because runway shapes everything. At six months, M&A is already in distressed territory and buyers know it. At twelve months, or near profitable, buyers will pay a fair price or better.

The second is whether the business model is viable. Being profitable or on a clear path to profitability opens up options and buys time, because a business with positive unit economics has leverage in any conversation that a cash-burning business doesn't.

The third is where your team and stakeholders actually stand. Co-founders, key team members, and investors all need to want the same outcome, and that matters as much as whether the strategy itself is right. Tom added the legal dimension, which is that founders have obligations to their investors, and whichever path they pick needs to be executed without putting the founder personally at risk.

Get in Touch

Harbottle & Lewis advises venture-backed and emerging companies on the legal side of everything covered in this post, from M&A and shareholder agreements to director obligations. If you'd like a confidential conversation with Harbottle, please reach out to Tom Macleod.

23mile works with venture-backed founders considering their options outside the traditionally scale to IPO path. We provide M&A advisory, restructuring support and invest directly in B2B, revenue generating UK-based startups with a stable customer base. We also support VCs who are considering unlocking liquidity in their portfolios. Get in touch for a no-strings confidential conversation.